picture alliance / NurPhoto | Jakub Porzycki

Studie

Staying focused: Priorities for transatlantic China policy coordination

Input Report for the China Track at the Munich Security Conference 2025

Introduction

By Bernhard Bartsch

This report aims to chart a way forward for the coordination of transatlantic China policies at the outset of the second Trump presidency.

The United States and EU both recognize China as a political, economic and technological challenge and, increasingly, as a threat to national and global security. China policy has had a heightened role in transatlantic relations in recent years, generating a remarkable convergence, based on the conviction the United States and Europe have a shared interest in addressing the challenges emanating from China jointly. This assessment was deepened by China’s substantial support for Russia’s war against Ukraine, ongoing Chinese market distortions and intense competition to control disruptive technologies, notably Artificial Intelligence (AI).

Fundamental policy shifts in Washington can be expected to test the transatlantic relationship again. This report therefore outlines a pragmatic China policy approach designed to keep the focus on three key areas for tackling the China challenge: transatlantic burden sharing, dealing with market distortions and technology controls. It also points out tremendous risks for both the United States and Europe should a coordinated transatlantic China policy fail.

Bracing for disruption

As the second Trump presidency begins, the whole world is bracing for turbulence. It seems certain to include disruption in the triangular relationship between the United States, the EU and China.

Before taking office, President Donald Trump signaled the United States would not be bound by precedents, established commitments or even international law (threatening invasions of Greenland or the Panama Canal). He has since raced to live up to his disruptor image, by leaving the Paris Agreement on climate change and the World Health Organization (WHO) and raising tariffs against Mexico, Canada and China.

The EU and its member states (and other G7 partners) are frantically discussing approaches to dealing with the new Trumpian era. However, political uncertainties within the EU are undermining the bloc’s strategic thinking and coordination. Germany and France are struggling to find stable political majorities, with rising right-wing populist parties enjoying a MAGA tailwind. The new European Commission has an ambitious agenda to restore European competitiveness and establish the EU as a relevant geopolitical actor. However, its initiatives will only be as strong as the member states’ collective will to pursue them.

China’s leadership appears unfazed, externally at least, by another four years of Trumpian China policy. President Xi Jinping is continuing to accelerate China’s military build-up, strengthen ties with Russia, upgrade Chinese industrial capacity and push for technological independence and leadership in strategic sectors.

However, this comprehensive policy push cannot mask China’s serious socioeconomic challenges, so President Xi is turning up the volume on his longstanding call to be ready for “struggle”.

While the US finds itself in a far more existential rivalry with China, the EU’s “derisking strategy” demonstrates a significant convergence on national and economic security and technology controls. China displays frustration with this development by regularly accusing the EU of merely acting on Washington’s behalf, a view rebuffed by Europeans who highlight uniquely European interests at stake. Still, the 27 EU member states hold divergent views on de-risking. A disruption of the transatlantic relationship could push Europe back to less risk-aware engagement with China.

Staying focused

Transatlantic convergence on China since the first Trump administration has been based on a recognition that both sides of the Atlantic have a strong interest in working together, despite different starting points and strategic priorities. The convergence has been driven by:

- A joint sense of urgency to counter Chinese challenges to the global order, economic stability and security

- Recognition that “factoring in” China would put other disputed issues into a broader context and help to find common ground

- Joint political will to make China policy a priority within broader transatlantic cooperation

- Closer exchange of information, research and analysis leading to a shared mainstream understanding of China and the challenges posed by its political agenda

- Structured political dialogues and consultations to create alignment.

Based on these factors, transatlantic China policy has been shaped by specific action areas. In 2021 and again in 2023, MERICS, the Munich Security Conference and the Aspen Strategy Group published reports identifying priorities for transatlantic cooperation on China. The reports identified seven priorities for action:

- Pushing for an economic level playing field

- Advancing shared economic security and retaining the technology edge

- Providing alternatives on infrastructure and connectivity

- Engaging China on combatting climate change

- Setting the agenda in international institutions

- Preserving liberal society and promoting human rights

- Maintaining a balance of power for a free and open Indo-Pacific

The seven action areas have not lost any of their relevance or urgency. Nevertheless, given the priorities of the second Trump administration, only three items have a realistic chance of remaining high on a transatlantic agenda, and with an adjusted focus:

- The “level playing field” agenda must now focus on market distortions created by Chinese industrial overcapacities

- The discussion about the balance of power in the Indo-Pacific has become a debate about transatlantic burden shifting

- Concerns about economic security and retaining the technology edge have only intensified, especially around semiconductors and AI regulation

Much can be gained by keeping these three areas as the focus of joint transatlantic policymaking. It is an agenda that aims to protect common interests by safeguarding global security and stability, ensuring open markets and fair competition and keeping a lead in critical technologies, in particular AI. It also protects the status of the United States as the leading military power.

Updating the priorities for transatlantic China policy coordination

Transatlantic burden shifting: The trade-offs between European and Indo-Pacific security

The United States and Europe have different threat perceptions. While Europe sees Russia as an existential threat, the pacing threat for the US is China. Deterring China and ensuring stability in the Indo-Pacific is Washington’s overriding strategic priority and European have long been alerted that they will have to take greater responsibility for their security, to enable the US to pivot resources towards Asia. In recent years, the American request has moved from “burden sharing” to a substantial “burden shifting”, as Liana Fix and Abigaël Vasselier write.

For now, Russia’s war against Ukraine is keeping the United States deeply engaged in Europe, and China’s support for Russia is demonstrating the interlinkages between the Europe and Indo-Pacific theatres. But President Trump is already pressing Europeans to drastically increase their defense spending and has even threatened to leave NATO, a drastic move that would destabilize the global security architecture. Russia would benefit hugely, as would China and its fledgling security-focused institutions such as the Shanghai Cooperation Organization (SCO) or the Global Security Initiative.

The imminent challenge facing the United States and Europe therefore is to agree over the parameters and conditions for burden shifting. They need to focus on a managed transition to a new form of transatlantic security cooperation that affirms the interlinkages between Europe and the Indo-Pacific. Successfully and jointly countering Russia’s expansionist ambitions in Europe would go a long way to building deterrence against China’s security and systemic threats in the Indo-Pacific and beyond.

Priorities for action

- Developing a common assessment of the implications of strategic competition with China

- Setting realistic parameters and conditions for transatlantic burden shifting around a managed transition to a new form of transatlantic security cooperation that acknowledges the interlinkages between Europe and the Indo-Pacific

- Building broad-based deterrence towards China, combining different tools available to the United States, Europe and other G7 and like-minded partners

- Working to convince China to scale back its direct and indirect support for Russia’s war against Ukraine

Market distortions: Transatlantic coordination is key to tackle China’s overcapacity-driven export flood

China’s exported overproduction is an established source of troubles in global markets. Overcapacities are driven by China’s very economic model and threaten companies on both sides of the Atlantic. The market distortions emanating from China, (which has one third of global manufacturing) are a problem far beyond US and EU home markets. They also distort third markets, where US and EU companies struggle to compete with made-in-China products, and impact more advanced manufacturing like solar panels and electric vehicles (EVs). The effectiveness of solo efforts to protect markets is limited, but transatlantic cooperation could effectively double the undistorted market, benefiting US and European companies alike, write François Chimits and Jacob Gunter.

There is a risk of relatively minor frictions in the transatlantic economic relationship taking precedence over far greater shared problems with China. Taking coordinated action against Chinese market distortions could tilt the cost-benefits of China’s subsidies and may push Beijing towards a cooperative solution further down the road.

Priorities for action

- Put the focus on sectors and distortions with the greatest convergences, such as critical raw materials or steel and aluminum

- Pursue multiple forms of coordination, from soft, ad hoc sector-specific agreements to firmer actions on jointly-agreed upon risks

Technology controls: Bridging the transatlantic gap in technology protection

Ensuring that like-minded democracies stay ahead in tech is more urgent than ever, given how the rapid evolution of technologies like AI is reshaping geopolitical, military and economic power. The securitization of technology is bearing down on many commercial sectors (from EVs to foundational semiconductors) and has global implications for economic development and the green transition, write Rebecca Arcesati and Antonia Hmaidi.

Washington sets the agenda, taking a national security focused approach, while Europeans tend to have fewer concerns about cooperation with China. Nonetheless, powerful US export control authorities with wide extraterritorial reach put constraints on how far Brussels and the EU 27 can set their own terms economic and tech relationships with China. The European Commission’s pressure for an effective export control strategy has improved coordination among the EU 27, but Brussels can do little more without backing from national capitals.

Europeans need to strengthen intra-EU coordination and build technical capabilities, while the US should clearly delineate national security objectives so the transatlantic alliance can address shared security concerns over technology. Without this, there is a real risk the United States might lose Europe’s support for its work to address the genuine national security risks stemming from China’s technological might. Alienating Europe might push it towards greater cooperation with China on critical technologies – an outcome unlikely to be in anyone’s interest, except China’s (and possibly Russia’s).

Priorities for action

- For the US, clarify the export control agenda’s precise national security objectives, with clearer distinctions between commercial and national security objectives and a more coherent approach to licensing

- For Europe, develop a cohesive and proactive framework for technology export controls

- Maintain a transatlantic coordination format for the nexus of trade, technology and national security such as the Trade and Technology Council (TTC)

The risk of losing focus

Even with a well-aligned transatlantic (and G7) China agenda, the United States and its allies would face severe challenges. China’s leadership is astutely focused on countering all Western efforts to constrain its rise. As part of this, China is increasing its global diplomatic footprint through groupings such as BRICS, the SCO, various initiatives and a multitude of bilateral agreements with countries in the Global South. Although China’s leadership faces multiple structural problems at home, it believes in its ability to make advances in the areas most central to China-US rivalry:

- The People’s Liberation Army (PLA) is continuing a massive military build-up to challenge US dominance in the Pacific and prepare for possible conflict over Taiwan.

- China’s record exports in 2024 showed it making inroads into Western as well as third markets for high-tech products and technologies that can disrupt strategic industries (such as autos or green tech) and dominating third markets.

- China is stepping up efforts to attain technological self-reliance. US export controls have proved painful, but it is unclear if China’s progress can be slowed down. Visible successes such as DeepSeek give the impression that even if China is not yet winning the tech war, it is not losing it either

Such perceptions will matter. With great uncertainty and disruption emanating from the United States, China is now trying to establish itself as an anchor of stability. Although the next few years are unlikely to resolve US-Chin strategic competition, they may well be decisive for how others perceive the trajectories of the great owers. Political and economic actors around the world are currently hedging their bets but may not be able to do so forever.

A well-coordinated transatlantic China policy can do a lot to build momentum for the joint interests of the United States, Europe and like-minded partners. Alternatively, rifts in the transatlantic partnership would add credibility to Beijing’s narrative that the East is rising, while the West is in inevitable decline.

1. Transatlantic burden shifting: The trade-offs between European and Indo-Pacific security

By Liana Fix and Abigael Vasselier

Political and military leaders on both sides of the Atlantic face fresh security challenges from interlinkages between European security and Indo-Pacific stability. North Korea’s decision to send around 10,000 elite soldiers to fight alongside Russian troops against Ukraine is the latest, starkest linkage between the Asian security space and the Euro-Atlantic one. However, China, North Korea and Iran have all stepped up their support for Moscow’s war of aggression, providing Russia with an enabling mix of economic support and military capacity that threatens European security. Both sides of the Atlantic recognize the two theatres are increasingly linked, but how these interlinkages should be addressed is contested.

Europe and the United States see the strategic environment and objectives differently

The United States and Europe have different threat perceptions and see different root causes of the interlinkage problem. For European leaders, Russia’s invasion of Ukraine underscored that Russia remains the foremost existential threat to peace in Europe. But Europeans were slower to recognize the global dimension and interlinkages between the Ukraine war and Indo-Pacific stability, and especially China’s hand in supporting Russia’s war. They are only reluctantly coming to the realization that China’s increased meddling in European security and Russia’s pact with North Korea and Iran has the potential to transform the landscape of European security and European strategic culture. Whether and how far Europe should recognize China as a security threat for the Euro-Atlantic space, and the consequences, are not sufficiently discussed among Europeans.

For the United States, on the other hand, China is the pacing threat, and deterring China and ensuring stability in the Indo-Pacific has become a core national interest and overriding strategic priority. Russia is seen as a less relevant threat (some would even doubt about the nature of Russia as a threat) and increasingly an offshoot of the China problem due to its dependence on China. Among the Washington establishment, including parts of the new Trump administration, the primary concern is not Russia, but that deterrence with China over Taiwan could fail. They fear the United States would be overstretched by (and possibly lose) a two-front war in Europe and the Indo-Pacific. Both Democrats and Republicans therefore want Europeans to shoulder more of the burden for European security.

There is a strong desire to shift more US resources to the Indo-Pacific in a context of limited US spending and macro-economic pressure. Meanwhile, Europeans fear the consequences of the shift in US priorities. They worry that, especially under President Donald Trump, US security guarantees for Europe will not be ironclad, and that Europe will be left alone dealing with Russia if the United States is distracted by a conflict over Taiwan. At the same time, Europeans will not be able to stay on the sidelines of such a conflict. Their immediate economic interests will be affected.

Due to limited resources, maintaining security in Europe and stability in the Indo-Pacific will not be possible without trade-offs for the United States and for Europeans. Choices need to be made on both sides of the Atlantic about how to deal with the new security reality in Asia and in Europe, who shoulders which part of the burden, and how the new modus vivendi will look like: either constructive joint preparedness or erratic separate decision making under pressure of events.

Burden shifting will take place but pace, timing, and scope will matter

Since President Barack Obama’s “Pivot to Asia” policy in 2011, Europeans have understood that US foreign and security policy would focus on challenges stemming from Asia. The past two US administrations have developed a bi-partisan view on China, albeit around two differing objectives of “winning the strategic competition” and maintaining “co-existence” with China. The EU has responded to Washington’s new focus with a complex strategy on China that would mix realist engagement and a more consequential approach on the systemic challenges (from economics to security) that China brings along in Europe and abroad. The EU’s strategy on the Indo-Pacific was adopted by member states, and Europe developed security and economic alliances in the region. However, there is a limited European consensus regarding China as a security challenge for Europe, despite Beijing sustaining Moscow’s war machine. Nor is there any clarity on likely US demands for a European security presence in the region – whether in peacetime or facing an escalation.

US strategic thinkers and policymakers mostly agree the United States would lose its hegemonic global position if it were to fail to deter China in the Indo-Pacific, hence their growing concern about the viability of sustaining both theatres and need to prioritise the Indo-Pacific. Some therefore suggest not only to share the burden of European security with Europeans, but to shift the burden: To give Europeans substantially more responsibility for their own security for the US to focus on the Indo-Pacific. For that, Washington expects Europeans to spend much more for their own defense and at the same time to align with US China policy, especially on economic policy. This is where Europe has leverage and can bring something to the table on the question of trade offs. But there is concern whether Europe is capable of ensuring its own security, in terms of military technology required, political willingness to increase defense spending and speed to acquire the necessary equipment.

While some in Washington would agree that the best deterrence to China would be to show that the West can win the war in Ukraine, this is not recognized by all. Questions over how much US capacity will remain in Europe, the speed of US rebalancing and the degree of European involvement in reshaping its security environment are therefore discussed controversially. Different approaches have emerged in US thinking on how to shift resources from Europe to the Indo-Pacific. These different scenarios will largely depend on the nominations and the first decisions and deals made by the Trump administration, including with Russia, Europe and China.

Approach 1: A unilateral US retreat from Europe

This is the European side’s greatest fear, a unilateral retreat or sudden abandonment by the United States, which could take different forms:

- A unilateral US policy decision to withdraw the majority of US troops from Europe, or in the worst case, to withdraw the US nuclear umbrella, suddenly leaving Europeans without security protection.

- A contingency in which the US does not honor its NATO Article 5 obligations and abandons Europe and NATO at a time of conflict.

- A withdrawal and shift to the Indo-Pacific of crucial US capabilities needed for European security (strategic enablers) without giving Europeans time to prepare and to produce their own replacements and alternatives.

- This scenario would lead to a serious disruption of the defense industrial cooperation between Europe and the United States. The US would come to lack the European market for their arms sales and the capacity to invest and transform their military base to be able to deal with the Indo-Pacific. At the same time, Europe would lack the high-technology military equipment needed to win the war in Ukraine and have real deterrence capabilities for the future.

Approach 2: A managed transition with transatlantic cooperation

A managed transition would include an agreed NATO timeline (anything from five to 25 years) for Europeans to replace critical US capabilities with their own capabilities and forces and thereby free up US resources for the Indo-Pacific:

- Europeans would be part of the process. They would need to commit to substantial defense spending increases and investment within a relatively tight timeframe. This would need joint European action, despite inner-European divides.

- The United States might abandon the timeline in a security emergency, leaving Europeans exposed as their defense industries need time to scale up.

- This scenario would allow for the development of a further integrated transatlantic industrial defense base, allowing Europe to acquire the technologies it misses today. This, however, would entail that Europe continues to be largely dependent on US military technology and investments.

- The US role in NATO would be diminished but not dormant.

Approach 3: Adaptations to the status quo

In this approach, any radical reshaping of the transatlantic alliance and the current burden sharing model is rejected, and changes limited to adjustments to the status quo, such as:

- An increase in European defense spending to at least three percent of NATO members’ GDP, withdrawal of the 20,000 US troops stationed in Europe (2022 data) and their replacement by European troops, a “European pillar” in NATO and a European Supreme Allied Commander Europe (SACEUR).

- In this scenario, the United States would opt for only adjustments to the burden sharing status quo, driven by the fear of losing European allies in its strategic competition with China and effort to maintain global hegemony if it pushed too hard on a more radical burden shifting agenda.

- In this scenario, the United States would encourage European investments in its defense industrial base, but European overall dependency on the United States would remain the same as today.

Approach 4: A mix of erratic decisions, factional infighting and outside contingencies

The US administration may pursue a mix of erratic decisions, driven by different interest groups competing in the White House in the absence of a common framework and objectives for European and Indo-Pacific security. A dichotomy stemming from infighting between rival factions of trans-Atlanticists versus restrainers / China prioritizers could be multiplied by sudden developments and contingencies in Ukraine, Taiwan, or the regions.

- Such a haphazard course of action risks alienating European and Indo-Pacific partners and leaving Europeans on to take decisions on future European security alone.

- The potential upside of infighting and erratic decision making is that it would create an unpredictability in US policy towards China that can give the United States leverage. Beijing’s priority at this stage is to maintain stability in its relationship to the US. while the new Trump administration sees a window of opportunity in the next five years to win the strategic competition with China. This can put Beijing on the back foot.

- But of course, this also means a volatile relationship prone to risk and escalation. And it would leave Europe with a lack of direction and difficulties to plan and act, which could allow Russia to exploit uncertainty for its own benefit.

- It would leave Europeans in a difficult position to invest political capital in building an integrated defense industrial base.

From all these four approaches outlined above, it has yet to be seen which approach will prevail, and whether and when the Trump administration will adopt a coherent strategic framework towards burden-shifting and trade offs between European and Indo-Pacific security that the interlinkages between both theatres would require. Europeans and Indo-Pacific partners alike will need to discern the contours of any US emerging approach, which may not prove easy.

Conclusion: Europe needs to be ready for all scenarios

Divergences within the transatlantic allies’ understanding of the strategic environment and its interlinkages are leading to differing priorities, capabilities and timeframes.

Europeans are sobered by Trump’s victory and realistic about Washington’s strong messaging that Europe needs to take far greater responsibility for its security. No one doubts that burden shifting will take place. Debate has moved on from the need for European nations to reach the defense-spending above the threshold of two percent of GDP coupled with pleas for US recognition of European contributions beyond military spending to a much more robust discussion of everything up to 5 percent. There are indications that President Trump does not intend to withdraw from Europe suddenly and fully. The real challenge is for the United States and Europeans to agree over the changed parameters of burden sharing.

China will be at the heart of trade-offs between the transatlantic partners. The Trump administration is likely to demand economic and trade alignment on China in return for US contributions to Europe’s security, which will tie the US and Europe closer together, if Europe follows suit and adopts a tougher China policy. This is where Europe has significant leverage and can be a net contributor to the US dilemma of a two-front conflict, through economic measures (which does not exclude European military contributions to the Indo-Pacific). European and US actors will have to get the mix right of a division of labor in Europe and the Indo-Pacific, and Europe will have to develop stronger “cross-theater awareness ”.

For Europe, it is urgent to recognize that this debate on burden shifting will shape its future security architecture and defense capabilities. It needs to be transformed into an opportunity to shape a coherent and solid defense industrial base sustained by a political leadership willing to shoulder the lion’s share of European security. This would also open the space to address the shortcomings in transforming the European-US defense industrial base cooperation and addressing the technological gap that Europe is facing to deter Russia and ensure peace on its Eastern front.

Developing a common assessment of the implications of the strategic competition with China and the trade offs with European security together with the new administration will help to address the interlinkages between deterring China in the Indo-Pacific and deterring Russia in Europe. Moving towards the recognition of China as a threat to European security in the context of the war in Ukraine is becoming an urgency for the Europe. Furthermore, the EU and European states will need to ensure they are at the table for a peace plan in Ukraine, to protect the credibility of future deterrence. For this reason, security issues which will continue to be addressed in NATO need to be increasingly discussed within the European Union to empower the European Commission to break silos between economic and security issues, increase synergies with NATO and develop a security and defense vision for Europe.

2. Market distortions: Transatlantic coordination is key to tackle China’s overcapacity-driven export flood

By François Chimits and Jacob Gunter

China’s 2024 trade surplus shattered records at USD 992 billion as the products of its over-investment, overcapacity, and over-production poured into global markets. Tackling the imbalances generated by its economic model is difficult. At best, solo efforts may only protect a single internal market from the warping effects. Rather than leaving companies on either side of the Atlantic protected from Chinese overcapacities only within their own home market, transatlantic cooperation could effectively double the undistorted market – amounting to about 15 percent of global GDP by purchasing power parity (PPP) each.

The risk is that small issues in the transatlantic economic relationship will take priority over far bigger shared problems emanating from China. Both the EU and United States accuse each other of distortive subsidies, market access barriers, and unfair procurement practices, all of which exist. However, both face the same issues with China on a much vaster scale. The most authoritative estimates put China’s annual state support to production at around 2 percent to 5 percent of GDP, compared to less than 0.5 percent (at most) in OECD countries. Furthermore, the market-warping emanating from China, which now has one third of global manufacturing, is not only a problem in US and EU home markets. It is also distorting third markets, where US and EU companies will struggle to compete with made-in-China products.

The US and EU should shun the false equivalencies implicit in tit-for-tat suggestions that the other distorts markets as China does. To put it simply - If we cannot find solutions to our minor problems and build political will to address China, only small slivers of global market share will remain.

Unchecked, China’s overcapacity is set to overwhelm both sides of the Atlantic

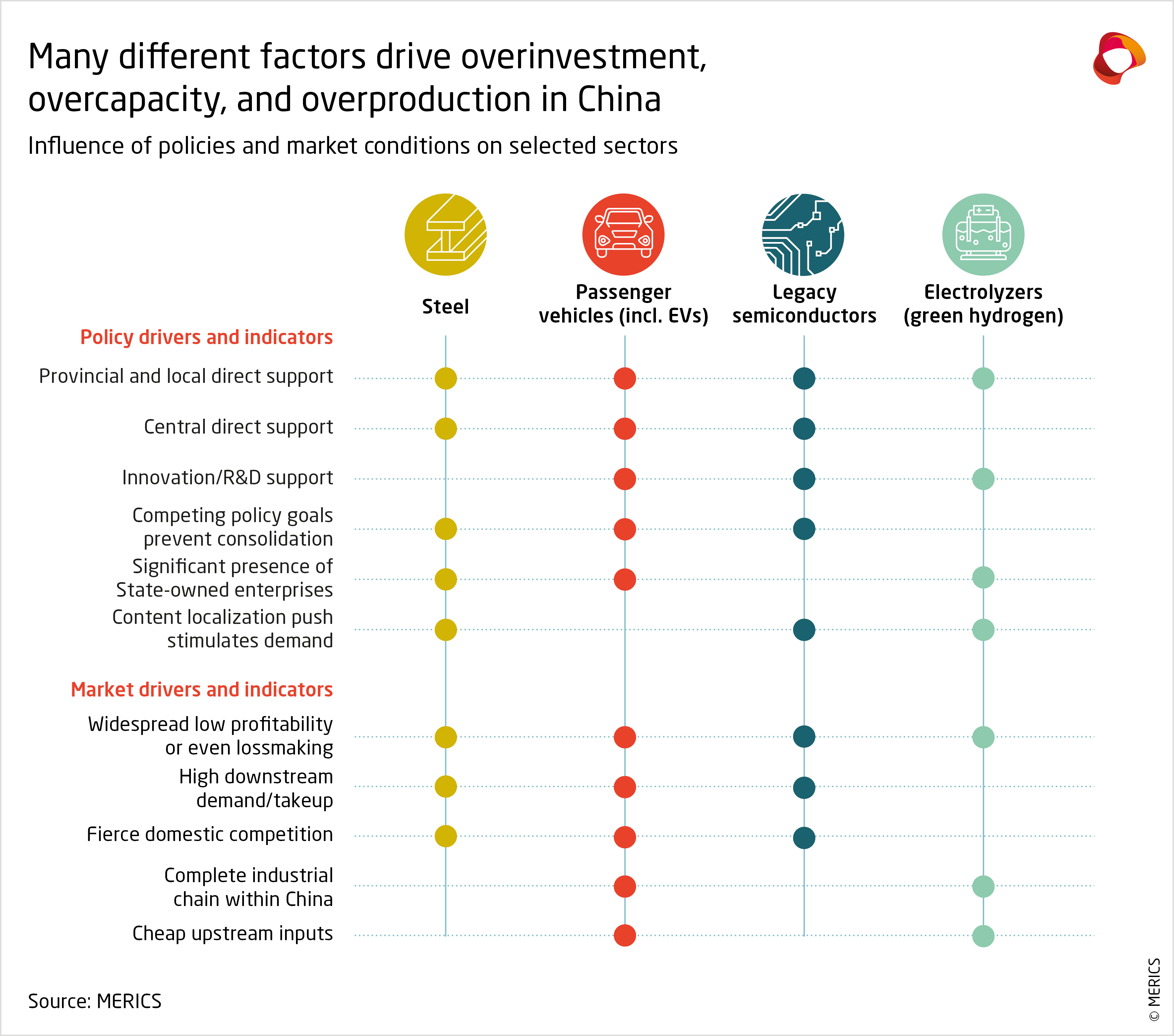

China’s very economic model under President Xi Jinping is driving the overcapacity warping global markets, and the effects are a risk to each side of the Atlantic. China’s exported overproduction is an established source of troubles in global markets for traditional primary industries like steel, aluminum, glass, and basic chemicals. Now, it is warping markets for more advanced manufacturing like solar panels and electric vehicles (EVs). Many factors driving overcapacity in those sectors exist in others.

Similar effects may be germinating, or predictable. MERICS recently published a deep study of ongoing and future overcapacity risks in China, looking at steel, passenger vehicles, legacy-node semiconductors and electrolyzers for green hydrogen. We found common and distinct drivers and indicators of excess production in China.

Crucially, many of the factors shared in several of these case studies also exist in sectors where blatant overcapacity is not yet present, signaling they may already meet the conditions for overproduction to emerge.

In the short to medium term, this includes;

- Legacy semiconductors (varied by type),

- Lower to mid-range medical devices,

- Pharmaceuticals,

- Low to mid-range industrial machinery and components,

- IT equipment

In the longer term, conditions are moving in the direction of overcapacity in sectors like;

- Electrolyzers

- Advanced medical devices

- New materials

- Advanced industrial machinery and components

Left unaddressed, the warping effect of China’s expanding overcapacities risks undermining prices worldwide, and North American and European exports. This could confront US and European firms with serious problems, as they have a legal duty to shareholders to maximize returns and profits. Chinese firms face ono such pressures under President Xi’s “New Era” and commitment to “Chinese -style modernization”, which tolerates anemic profitability and even outright lossmaking.

Washington favors national security, while Brussels focuses on level playing fields

Washington’s actions to shield the US market from Chinese distortions have mostly been taken on national security grounds. The first Trump Administration generally described its embrace of expanded tariffs on Chinese goods entering the United States as countering unfair trade practices, intellectual property theft and technology transfer requirements. The national security justification for barriers against China-made goods became yet more dominant under the Biden Administration. Biden’s Chips Act curbed exports of advanced semiconductors to China; his Inflation Reduction Act offered hefty subsidies to manufacturing investment with “no-China” elements in their value-chains; barriers were raised against Chinese-made EVs. All these actions were justified, formally and narratively, as protecting US economic security. Although some measures were taken under “level playing field” (LPF) instruments (those against EVs, solar panels, minerals, ship-to-shore cranes, medical products, legacy chips and solar panel inputs), they were enshrined in a security narrative about dependencies and resilience.

In less than a decade, US average tariffs on incoming Chinese goods have jumped from 3 percent to 20 percent, excluding the non-tariff-based measures mentioned above. National security-based measures, and the US legal framework in general, favor more reactive and substantial tariffs, which are aimed both at mitigating the discovered distortions, and at preventing the entry of Chinese products on the US market. They tend to have a more limited burden of proof than more regulatory measures.

China’s share of direct US imports has therefore fallen, from 23 percent in 2017 to 13 percent in the first half of 2024. Some of this is because the final production stages have been diverted to intermediary countries to avoid tariffs. Nonetheless, the trend for partial decoupling is real.

The EU approach has focused more tightly on market distortions and is gaining pace. Brussels has modernized, streamlined and extended its toolbox of measures to level the playing field and ramped up measures against China-made goods. Its EV tariffs impacted around 10 billion dollars of potential annual imports. Brussels also initiated 26 LPF measures on Chinese products, 87 percent of such EU measures in 2024. In the previous decade it took on average 16 such measures, of which 6 percent were about Chinese products.

As these actions are based on the EU’s regulatory mindset (part of the single market’s core mandate), they are geared solely at redressing the identified distortion. Diversification obligations and national security measures are in their infancy at the EU level. The barriers are therefore pitched lower than those in in the US; additional tariffs on China-made EVs entering the European single market are set at 8 percent to 35 percent, whereas the US applies a 100 percent levy. As most EU measures were only initiated in 2024, any material diversification of Europe’s import base is not yet visible at a macro-level: China’s share within European imports is still rising.

Get by with a little help from your friends

In a globalized world, protecting a domestic market is no longer enough so co-ordination with partners is worth the effort, however complicated. For US or European firms, third markets are often as much an existential part of their business as their domestic ones. Furthermore, China’s industrial policies aim to climb the value-chain towards the knowledge intensive sectors OECD countries specialize in, so the EU and US face a common challenge from Chinese distortions.

The overwhelming majority of potential demand for Beijing’s favored advanced products is in the US and European markets. Any concomitant closing-up of those markets would seriously tilt the cost-benefits of China’s subsidies to such sectors, disincentivizing such actions and maximizing the appeal of a cooperative solution for Beijing further down the road.

We should not let perfect be the enemy of good. Ad hoc coordination on autonomous measures offers a way forward, given that US and EU approaches to Chinese distortions are unlikely to fully align. The EU will remain highly constrained by its regulatory and legal framework, less able to pursue the more discriminative and forceful measures available to Washington. Besides, the two sides of the Atlantic also have distinctive industrial preferences and specializations.

Given the added value of concomitant actions, the two sides would be better off accepting their unbridgeable divergences and focusing on sectors and distortions where their interests offer convergences. In steel, aluminum, green industries or even legacy chips, both have implemented barriers against Chinese-made goods, or are considering it.

Coordination can take multiple forms, from soft ad hoc sector-specific agreements to more constraining jointly-agreed upon risks, or distortion-free certificates across the board. Irrespective of the format, co-ordination would reduce the domestic costs of the measures, extend the depth of the distortion free market, increase the direct and political impact on Chinese industrial policies and encourage other like-minded partners to participate.

3. Technology controls: Bridging the transatlantic gap in technology protection

By Antonia Hmaidi and Rebecca Arcesati

Donald Trump’s re-election as president of the United States is likely to bring new challenges to already difficult transatlantic cooperation on China’s involvement in advanced technology. Some in Europe, including the European Commission led by President Ursula von der Leyen, share the US bipartisan consensus that sees China as challenging global security. However, European voices emphasizing the partner side of the China equation remain strong. Member states lack any consensus that containing China technologically – or, as outgoing US National Security Advisor Jake Sullivan put it, “keeping as large a lead as possible” over China – should be the strategy. In the absence of EU strategic alignment, Washington with its power over supply chains even beyond the US is in a strong position to foreground its major concerns.

Europe finds itself ill-prepared to navigate the confluence of three trends: 1) the arrival of a more unilateralist US administration; 2) the rise of extraterritoriality as an instrument of great power competition; 3) a growing technology partnership between China and Russia. Ensuring that like-minded democracies stay ahead is more urgent than ever as technologies like artificial intelligence (AI) are evolving fast and redefining the distribution of geopolitical, military and economic power. This challenge will require political will and investment on both sides of the Atlantic.

Trump’s decisions will greatly impact Europe’s relations with China in technology

As European capitals largely lack capabilities and capacity to systematically assess and act upon the China tech challenge, Washington readily sets the agenda, as was seen in US demands for the Netherlands and Japan to impose export controls on semiconductor manufacturing equipment. Powerful US export control authorities with wide extraterritorial reach constrain the ability of the EU’s 27 members (which retain sovereign authority on national security matters) to set the terms of their own economic and tech relationships with the world’s second largest economy.

Coordination among the EU-27 has improved to prevent undesirable transfers of dual-use emerging and foundational technologies to China and other destinations of concern. For example, several capitals have joined the “Wassenaar minus one” arrangement where like-minded partners have adopted harmonized export controls, particularly on quantum computing and semiconductors. Even reluctant capitals like Berlin now seem less eager to approve licenses for dual-use exports to China.

For Europe, the second Trump administration’s still-unknown approach to technology export controls is likely to present challenges. Although President Trump’s thinking on technology export controls has yet to be articulated, he is unlikely to abandon the fundamental tenets of strategic competition with China or weaken existing export controls significantly. Some analysts expect the Trump administration to pursue more extensive decoupling from China. However, strong tech industry representation in the new government – notably Elon Musk – makes predictions uncertain at best.

It seems likely that the new US administration will take a more erratic approach to tech policy, while being less willing than Joe Biden’s team to engage in lengthy negotiation with allies. The new team surrounding Trump is not unified in their judgement of the usefulness of export controls, as compared with tariffs, as an instrument to preserve America’s advantage in technology. Moreover, Trump demonstrated during his first term that his approach can be swayed by industry – and include concessions to specific companies, as seen with his final-hour effort to prevent Chinese-owned livestreaming app TikTok from being banned from the United States.

Trump arguably started the “tech war” during his first term by putting Chinese telecom giants ZTE and Huawei on the US Entity List of trade-restricted entities, only to then take ZTE off the list. Meanwhile, industry lobbying ensured that Huawei was still able to receive shipments of technology from many US companies, at least until licenses were finally revoked shortly before Trump left office. Even so, he reportedly pressed the Dutch government not to license the export of ASML’s most advanced chipmaking gear to China in 2018. We can expect some degree of inconsistency during his second mandate too.

Washington and Beijing are both turning towards extraterritoriality

As to coordination with allies, Trump’s track record and worldview suggest he may have more appetite than Biden for using the Commerce Department’s powerful extraterritorial authorities under the Export Administration Regulations (EAR), particularly the so-called Foreign Direct Product Rule (FDPR). This rule allows the US government to require that non-US exporters of non-US technology apply for a US license if the product in question either contains or was made with any US technology. As few high-tech products are completely without elements of US technology, the rule could theoretically apply to most of them. During the first Trump administration, the FDP rule was applied to Huawei to prevent Taiwan’s TSMC from fabricating chips for the Chinese tech giant. Instead of negotiating with, say, Germany to limit future exports of components for chipmaking equipment to China, Trump might present German industry with a fait accompli.

The Biden team was extremely innovative on export control policy, putting in place sophisticated and powerful tools that the incoming administration could now choose to use. Among these is the October 2022 package that for the first time limited the export of chips based on a performance threshold to an entire country instead of the prevailing company-by-company approach. Recent limits to the global diffusion of advanced AI systems through controls over the underlying computing power are another example.

Meanwhile, Beijing too is stepping up efforts to expand its extraterritorial jurisdiction, with potentially far-reaching consequences for global technology supply and value chains. China has built up a unique regulatory regime for export controls whose remit reaches beyond military and dual-use technology. Beijing has begun to apply this regime more proactively and flexibly, especially for critical minerals. Moreover, China’s new implementing rules for dual-use export controls include extraterritorial authorities that mirror the US’s FDPR. It is unclear if Beijing will be able to enforce the new rules as the vigorous weaponization of supply chains could hurt Chinese companies. Chinese technology is not (yet) omnipresent in high-tech products the way US technology is.

Both Beijing and Washington increasingly perceive each other mainly through the lens of great power rivalry. Any digital technology from the other is seen as a risk, as the United States has demonstrated with its ‘ICTS’ rules, covering information and communications technology and services. If implemented, some of these rules could prevent European carmakers from selling to the US market if their models embed any Chinese (or Russian) hardware or software. For instance, Volkswagen (VW) has built up its China footprint in software for self-driving cars with the aim to jointly develop software across China and Europe. With the new rule, VW will not be able to sell cars with this software in the US. To be sure, VW is already bifurcating its tech stack by betting on local partners in both China and the US, effectively closing its in-house software development. But as many German car companies are localizing R&D to China, this rule is set to affect them more in the future. Elon Musk’s Tesla, which has separate supply chains for most key components, could serve as a model and is unlikely to be affected.

The same logic could be extended to many more technology stacks and supply chains. China’s longstanding campaign to build “secure and controllable” networks and information systems similarly views US digital technology as posing a risk to data and supply chain security. Europe should brace for a potential new phase of the US-China tech war, with greater costs and impact for its industries. Beijing is already pressuring carmakers to replace foreign chips with indigenous alternatives, and this is an area where European firms are still strong.

Both the US and Europe need to focus on greater clarity and cohesion

There is a real risk that the United States might lose Europe’s support in its efforts to address the genuine national security risks stemming from China’s technological might. The securitization of technology is affecting growing numbers of commercial sectors with global significance for economic development and the green transition, from EVs to foundational semiconductors. But a transatlantic wedge and a less competitive Europe would only benefit China.

The jeopardy created by China’s growing material support for Russia’s defense-industrial base could be overshadowed by European perceptions of a confluence of national security and commercial interests in the United States. Transatlantic frictions could obscure a topic that should be a top priority for US-EU cooperation over the next four years, given the scale of Western exports flowing into Russia via China that keep fueling Moscow’s war machine in Ukraine. This is an issue on which Europe should take the lead, as the Ukraine war is much closer to European countries than to the United States. Yet many capitals still view technology export controls and sanctions on China as a demand from Washington rather than something that is in their national security interests to pursue.

The Trump team should know that what keeps the United States ahead in competition with China is the strength of its alliances, which China cannot easily mirror. Alienating Europe could push it to cooperate more with China on critical technologies. Such an outcome is unlikely to be in anyone’s interest, except China’s (and possibly Russia’s). Washington should work to keep allies on board, which presupposes a clearer articulation of the of the US export control agenda’s precise national security objectives. Distinguishing more clearly between commercial and national security objectives would also help secure allies’ buy-in, as would a more coherent approach to licensing.

European capitals risk being increasingly forced to adhere to decisions made in Washington if they remain reactive and lack a clear and effective export control strategy of their own. The Commission has been pushing for such a strategy but cannot do much without capitals’ backing. The EU collectively needs a rethink of its approach to the nexus of technology, geopolitics and security, which also entails a drastic build-up of relevant competences in government. “De-risking” is an empty phrase without a clear assessment of the risks that are supposed to be mitigated and the resources to do so. Several European governments have built up economic security capabilities in the recent past, but most remain relatively weak on technology. Export control enforcement also remains difficult.

Trump’s transactional approach could provide Europe with an opportunity to advance its own interests, including on bilateral and plurilateral coordination of export controls. But to work with the circumstances, Europe needs to be aware of its own leverage and willing to negotiate. This also presupposes an acknowledgement that the EU will continue to have far more leverage than individual countries, including the bigger member states.

To bridge differences, sustained US coordination with European capitals will be just as important as coordination with Brussels. The Biden administration’s outreach on technology and national security focused on the European Commission and on a few countries on an issue-by-issue basis – for instance, engaging with the Netherlands on semiconductors. The Trade and Technology Council (TTC), a transatlantic coordination format devised for this new nexus of trade, technology and national security, suffered from weak buy-in by national capitals, even though it did help coordinate sanctions on Russia. The EU will itself require new formats that promote intra-EU unity on issues like export controls or the protection of strategic scientific and engineering know-how.

The evolving dynamics of transatlantic cooperation on China and technology highlight the urgent need for updated strategies from both the United States and Europe. As Washington adopts a more unilateral and potentially erratic approach under a new Trump administration, Europe must step up its efforts to develop a cohesive and proactive framework for technology export controls. This includes strengthening intra-EU coordination, building technical capabilities, and leveraging collective influence to navigate the dual pressure of US-China competition at the nexus of trade, technology, and national security. The US should step up dialogue and clearly delineate national security objectives to enable the transatlantic alliance to address its shared security concerns arising from technology.

Autor(en)

Lead Analyst (Büro Brüssel)

Leiter External Relations

Senior Economist (Büro Brüssel)

Fellow for Europe at the Council on Foreign Relations (CFR)

Lead Analyst

Senior Analyst

Leiterin Policy and European Affairs und Programmleiterin Internationale Beziehungen

Autor(en)

Lead Analyst (Büro Brüssel)

Leiter External Relations

Senior Economist (Büro Brüssel)

Fellow for Europe at the Council on Foreign Relations (CFR)

Lead Analyst

Senior Analyst

Leiterin Policy and European Affairs und Programmleiterin Internationale Beziehungen